Tax Planning Tips for Homeowners [2025]

Understanding Tax Deductions for Home Improvements

Home improvements can be significant investments, often leading to increased property value and comfort. Understanding the tax deductions available for these improvements can significantly reduce your tax burden. However, not all home improvements are eligible. Careful consideration of the nature of the improvement and its impact on the property's value is crucial. This knowledge allows you to strategically plan your home improvements to maximize your investment and minimize your tax liability.

Specific rules and regulations regarding home improvement deductions can vary based on the type of improvement and the specific tax code in force. Staying updated on these changes is key for maximizing the benefits and ensuring compliance with relevant tax laws. Consulting with a qualified tax professional is always recommended for personalized advice and to avoid potential errors or penalties.

Capital Improvements vs. Ordinary Repairs

A crucial distinction to understand is the difference between capital improvements and ordinary repairs. Capital improvements are enhancements that significantly enhance the property's value or extend its useful life. These are typically deductible. Examples include adding a new room, renovating a bathroom, or installing a new roof. Ordinary repairs, on the other hand, maintain the property's existing condition and are not deductible. Examples include repainting walls, repairing a leaky faucet, or replacing worn-out flooring. Understanding this distinction helps you properly categorize your expenses and determine which ones qualify for deductions.

Deductible Home Improvement Expenses

Several home improvement expenses qualify for deductions. These include expenses for additions to the home, such as new rooms or a sunroom. Improvements to existing rooms like kitchen or bathroom remodels also qualify. Installing energy-efficient windows or insulation can also contribute to a deduction. Furthermore, expenses for exterior improvements, such as a new deck or landscaping, might be eligible. Thorough documentation of all expenses is critical for supporting your deductions during tax season.

Maintaining Accurate Records

Maintaining detailed records of all home improvement expenses is paramount for claiming deductions effectively. These records should include receipts, invoices, and estimates. Categorizing expenses by type, such as labor costs, materials, and permits, further enhances the clarity and organization of your records. Keeping a running log of these expenses throughout the year simplifies the process of compiling the necessary documentation during tax preparation.

Seeking Professional Advice

Navigating the complexities of home improvement deductions can be challenging. Consulting a qualified tax advisor can provide invaluable assistance. They can guide you through the specific requirements and rules applicable to your situation. A tax professional can assess the eligibility of your improvements, accurately calculate your deductions, and ensure compliance with relevant tax regulations. This expert guidance ultimately saves you time, effort, and potential tax issues.

Mortgage Interest Deduction Strategies for 2025

Maximizing Your Deduction

Understanding the mortgage interest deduction is crucial for maximizing your tax savings. This involves more than simply knowing the amount of interest you paid; it encompasses careful record-keeping and a clear understanding of the types of interest that qualify. Properly documenting all mortgage-related expenses is essential for accurate reporting, ensuring you don't miss out on any potential tax benefits. It's also important to remember that the rules surrounding the deduction can be complex, and consulting a tax professional can provide valuable guidance tailored to your specific circumstances. This will help you avoid costly errors and ensure you're maximizing your deduction.

Furthermore, understanding the different types of mortgage interest that qualify is vital. While home equity loans and lines of credit often have interest that is deductible, it's crucial to differentiate them from other debt. Paying close attention to the specific terms and conditions of your mortgage is essential to avoid any surprises during tax season. This involves carefully reviewing loan documents and understanding the allocation of interest payments across various loan components. Careful review and understanding of these specifics can lead to a significant difference in your tax liability.

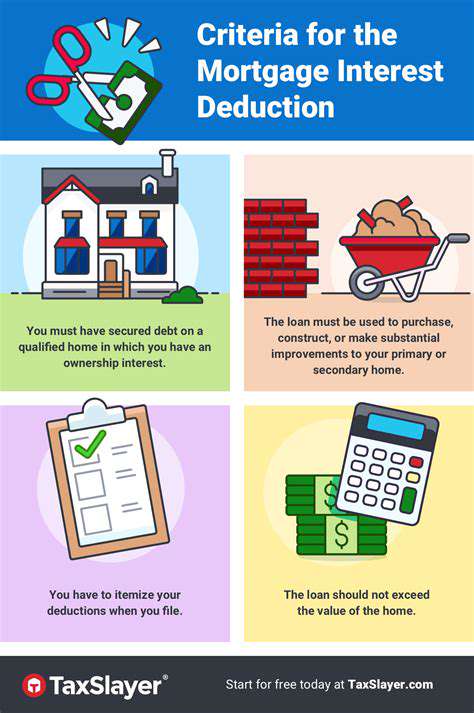

Understanding the Qualifying Mortgage

To qualify for the mortgage interest deduction, your mortgage must meet specific criteria. These criteria generally involve the property being your primary residence and the mortgage being used to finance the purchase or improvement of that property. This is a critical factor in the deduction process. Detailed documentation of your mortgage's terms and conditions, along with any supporting loan documents, is essential in demonstrating that the mortgage meets the eligibility standards.

The property must be your primary residence; it's not enough to simply own a property. Beyond simply owning a property, the mortgage must be directly related to that primary residence. This includes expenses like interest paid on the mortgage, property taxes, and any required homeowners insurance premiums. Furthermore, the mortgage must be held for personal use and not for investment purposes. Understanding and adhering to these rules is essential to ensure the validity of the deduction.

Strategies for Future Tax Planning

Planning ahead for your mortgage interest deduction is wise. One effective strategy is to carefully analyze potential future mortgage interest payments. This involves understanding the terms of any refinancing or new mortgage you might take out in the future. Anticipating these payments can help you proactively prepare your financial records for tax season. This detailed planning can help you avoid any last-minute scrambling or confusion.

Furthermore, consider the long-term implications of your mortgage decisions on your tax liability. A well-structured approach to understanding and managing your mortgage can significantly impact your future tax savings. It is wise to consult with a qualified financial advisor to discuss strategies that align with your long-term financial goals and tax objectives.

Adopting a balanced and nutritious diet can significantly impact anxiety levels. Prioritizing whole foods like fruits, vegetables, and lean proteins provides sustained energy and essential nutrients for optimal brain function. Reducing processed foods, sugary drinks, and excessive caffeine can help stabilize mood and reduce anxiety triggers. Incorporating foods rich in magnesium, such as leafy greens and nuts, can also play a crucial role in managing anxiety symptoms. This dietary approach isn't about strict deprivation, but rather focusing on mindful choices that nourish both body and mind, leading to a more balanced and resilient emotional state.

Property Tax Deductions and Strategies

Property Tax Deductions: A Comprehensive Overview

Property taxes are a significant expense for homeowners, but fortunately, there are often deductions available to lessen the financial burden. Understanding these deductions can significantly impact your tax liability. These deductions can vary based on your location and specific circumstances, so it's crucial to consult with a tax professional or refer to reputable tax resources to ensure you're taking advantage of all applicable deductions.

Understanding the different types of property taxes and the associated deductions is vital for maximizing your tax savings. This knowledge allows you to strategically plan your finances and make informed decisions about your property ownership.

State and Local Tax (SALT) Deduction

The State and Local Tax (SALT) deduction is a crucial aspect of property tax deductions. Historically, this deduction allowed taxpayers to deduct state and local taxes, including property taxes, income taxes, and sales taxes, up to a specified limit. However, recent tax legislation has significantly impacted this deduction.

The SALT deduction's limitations necessitate careful consideration of your tax situation. Understanding these limitations is crucial to accurately calculate your tax liability and avoid potential errors.

Residential Property Tax Deductions

Residential property owners often benefit from deductions related to their homeownership. These deductions can range from deductions for mortgage interest to property taxes paid. Understanding these specific deductions can greatly reduce your tax burden, and it is important to remain updated on any changes to these regulations.

Careful record-keeping is essential for claiming these deductions accurately. Ensure you retain receipts and documentation for all property tax payments and any related expenses.

Commercial Property Tax Deductions

Commercial property owners also have deductions available, though they may differ from those for residential properties. These deductions often involve more complex calculations and specific requirements.

Depending on the nature of the business and the specific property, the deductions available may include depreciation allowances and expenses associated with property maintenance and repairs. These deductions are crucial for commercial property owners to manage their tax liabilities effectively.

Strategies for Maximizing Property Tax Deductions

Several strategies can help maximize your property tax deductions. Careful record-keeping and organization of financial documents are essential for accurately calculating and claiming deductions.

Consulting with a qualified tax professional can offer tailored guidance on maximizing your deductions based on your specific circumstances. Seeking professional assistance is often beneficial to ensure you're taking advantage of all applicable deductions and avoiding potential errors or omissions.

Tax Laws and Regulations

Tax laws and regulations surrounding property tax deductions are constantly evolving. Staying informed about these changes is essential for claiming the most accurate and beneficial deductions.

Regularly reviewing tax publications and resources, or consulting with a qualified tax professional, can help you understand the latest updates and ensure that you comply with all regulations. Staying abreast of these changes is vital to avoid penalties or inaccuracies in your tax filings.

Tax Planning Strategies for Future Growth

Long-Term Capital Gains Strategies

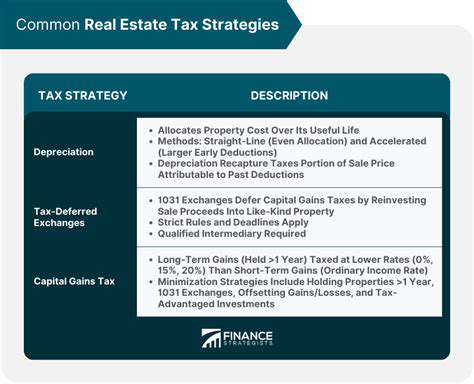

One crucial tax planning strategy for future growth involves strategically managing long-term capital gains. Understanding the tax implications of selling assets like stocks, real estate, or other investments is paramount. By carefully timing these transactions and utilizing available deductions and exemptions, homeowners can significantly reduce their tax burden while maximizing the potential growth of their portfolio. This proactive approach allows for a more significant return on investment, fostering sustainable wealth accumulation over time.

Capital gains taxes can vary significantly depending on the holding period. long-term capital gains, often applied to assets held for over a year, typically receive a more favorable tax rate than short-term gains. Homeowners should meticulously track their investment holdings and consider professional advice to ensure they are taking full advantage of these potential tax benefits and to avoid costly mistakes.

Tax-Advantaged Retirement Accounts

Utilizing tax-advantaged retirement accounts like 401(k)s, IRAs, and Roth IRAs is a cornerstone of sound financial planning for future growth. These accounts offer significant tax benefits, allowing contributions to grow tax-deferred or tax-free, depending on the account type. This deferral of taxes can lead to substantial savings over time and significantly boost retirement nest eggs. Understanding the nuances of each account type and how they align with individual financial goals is essential for optimizing returns and maximizing the tax benefits available.

Home Office Deductions

For homeowners who use a portion of their home for business purposes, claiming home office deductions can be a valuable tax planning strategy. This involves accurately calculating the portion of the home used for business and deducting expenses like mortgage interest, property taxes, and utilities. Proper documentation and accurate estimations are vital for a successful home office deduction claim. This deduction can significantly reduce the tax burden, especially for those operating businesses from their homes. Consult with a financial advisor or tax professional to ensure compliance with all relevant regulations.

Charitable Contributions

Strategic charitable giving can be a powerful tax planning tool for homeowners. By donating appreciated assets, homeowners can potentially reduce their taxable income and receive tax deductions. This strategy can maximize the impact of charitable contributions while minimizing the tax liability. Understanding the specific rules and regulations around charitable contributions is crucial for ensuring compliance and maximizing the tax benefits. Consult with a tax professional to determine the most effective strategy for your individual circumstances.

Estate Planning and Tax Implications

Developing a comprehensive estate plan is crucial for long-term tax planning. This involves considering wills, trusts, and other legal instruments to minimize estate taxes and ensure a smooth transfer of assets to beneficiaries. Proper estate planning can significantly reduce the tax burden on heirs and prevent potential legal complications. It's important to proactively address estate planning needs early on, working with an estate attorney to create a plan that aligns with individual goals and minimizes tax liabilities for future generations. This proactive planning can safeguard assets and ensure a more secure financial future for loved ones.

Read more about Tax Planning Tips for Homeowners [2025]

![Best Investment Strategies for Volatile Markets [2025]](/static/images/30/2025-05/StrategicAssetAllocation3AAdaptingtoMarketConditions.jpg)

![How to Buy and Sell Stocks [Beginner Steps]](/static/images/30/2025-06/ManagingYourPortfolio3ALong-TermStrategies.jpg)

Hot Recommendations

- Tax Planning Tips for Homeowners [2025]

- How to Get Insurance for a Short Term Rental Property

- Understanding the Benefits of a Roth IRA

- How to Manage Business Debt After a Downturn

- How to Use a Barbell Investment Strategy

- Best Ways to Track Your Progress Towards Financial Freedom

- Tips for Managing Credit Card Rewards While Paying Off Balances

- Tax Planning Tips for Stock Options

- How to Plan for Retirement if You Didn't Save Early

- Guide to Managing Legal Debt